Don’t let the sticker price of a camper van overwhelm you. You don’t have to pay it all at once.

There are several options for financing a camper van build. Whether you’re planning a custom build or considering a prebuilt model, how you structure the financing can make the investment much more manageable.

This guide walks through the main financing options for your van and build-out so you can compare approaches and choose what fits your plans.

Understanding the Real Cost of Van Life

The cost of van life usually goes beyond the van itself. Many buyers focus on the vehicle first, then realize the build details, upgrades, and gear significantly affect how the van needs to be financed. That is where financing considerations start to come into play.

Getting clear on those costs early helps prevent budget surprises later, whether you are planning a custom conversion or comparing prebuilt options.

Key Takeaways

- Financing a camper van build is usually split into two parts. The vehicle and the conversion are often financed separately.

- Prebuilt vans tend to fit more easily into standard lending categories. Completed conversions are typically simpler to finance than custom or in-progress builds.

- Build financing involves tradeoffs. Personal loans offer flexibility but often carry higher interest rates than vehicle loans.

- Mixed approaches are common. Many buyers combine loans and cash or phase build costs over time.

- Classification and documentation can affect approvals. How a van is categorized and documented often influences lender requirements and timelines.

The Two Parts of Camper Van Financing

Financing a camper van usually comes down to two pieces: 1) the van itself and 2) the build or upgrades that turn it into a complete custom build.

Depending on your financial situation, that may mean one loan, separate financing, or a mix of approaches. The van and the build are typically evaluated differently by lenders, which affects how and when each part can be financed.

Financing the Van Itself

When financing a camper van, the vehicle itself is usually the most straightforward part of the process. Many buyers start here before deciding how to handle build details or upgrades. That’s because the van is a completed asset with a clear market value, which lenders already know how to evaluate.

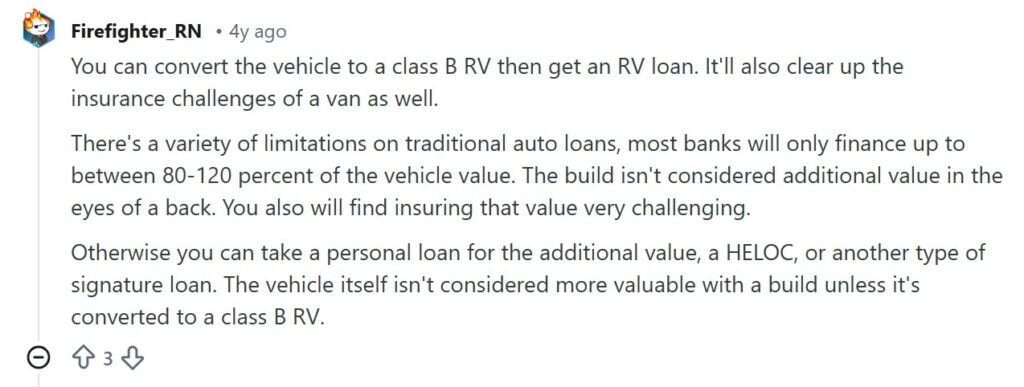

One of the most common ways to finance a camper van is through an RV loan. These loans are designed specifically for recreational vehicles, including qualifying camper vans and Class B models.

RV loans are offered by banks, credit unions, and online lenders. Loan terms often fall in the 15 to 20 year range, which many buyers find keeps monthly payments manageable.

Most RV loans require a down payment of about 10 to 20 percent of the vehicle’s purchase price. Loan length plays a big role in monthly costs. Longer terms usually mean lower monthly payments, but more interest paid over time.

Interest rates vary based on credit score, loan amount, and lender. Many buyers see rates around the 10 percent range, though offers can differ. Comparing lenders and getting pre-approved can help clarify your budget before moving forward.

Financing the Custom Build

Financing the custom build is less standardized than financing the van itself, largely because costs vary and the work may not be completed at the time of purchase.

If you’re planning a custom build or adding features to a prebuilt model, financing the conversion itself works differently than financing the vehicle.

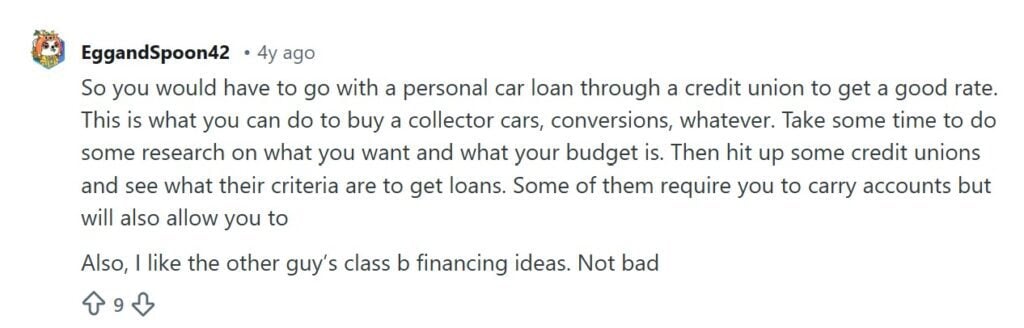

Build costs can be harder to finance through traditional vehicle loans, so many buyers turn to personal loans, pay cash, or use a combination of both.

Using Personal Loans for Build Costs

Personal loans are one way to cover build-out or conversion costs. These are unsecured loans, meaning they don’t require collateral like your van or another asset. This makes them a flexible choice for financing everything from solar panels to custom cabinetry.

Loan amounts typically range from $1,000 to $50,000, with terms between 2 and 7 years. Because these loans are unsecured, they often come with higher interest rates compared to secured loans like RV loans.

Interest rates can range from 5 to 36 percent, depending on your credit score and the lender. Borrowers with strong credit scores will generally receive better rates, making it worth comparing offers. The higher interest rate is one reason some buyers choose to put down a larger down payment to reduce the total interest paid over time.

Paying Cash for a Van Build

If you have the financial means, paying cash for your van or the build-out offers clear advantages. While financing can help spread out the cost, paying upfront can reduce long-term interest and leaves you owning the van and build outright from day one.

Combining Financing and Cash

One strategy that some buyers use is to finance the van purchase itself and then pay cash for the build-out.

This approach results in keeping monthly payments manageable while avoiding high interest rates on a personal loan for the custom build. It also provides the flexibility to work on the build in stages, without the pressure of a loan payment hanging over your head.

Real-World Financing Experiences

Van buyers and builders often share their financing experiences on Reddit and other online communities. During our review of recurring discussions, a few patterns show up consistently across different situations

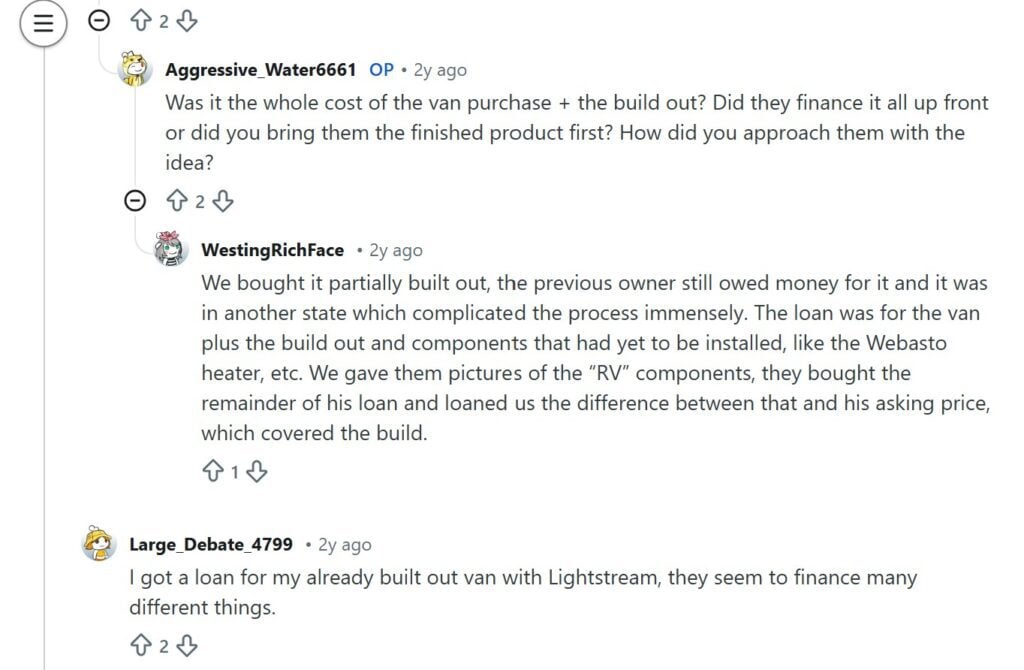

Financing is rarely a single loan

Most people finance the van first, then figure out how to handle the build separately. Some use personal loans for the conversion. Others pay cash in phases as the budget allows. Mixed approaches are common, not exceptions.

Prebuilt vans are easier to finance

Completed conversions like Geotrek’s Flatiron and Bear Peak qualify for standard RV or auto loans more easily than custom builds. Lenders are more comfortable with prebuilt vans because they have verifiable market values and often come with warranties.

Dealers can bundle the vehicle and conversion into a single loan, which simplifies the process. Custom builds, especially those still in progress, are harder to finance through traditional channels.

Build financing involves tradeoffs

Personal loans work for build costs, but the interest rates are typically higher than vehicle loans. Paying cash for parts of the build keeps things simpler. Some buyers phase the work over time to avoid taking on more debt upfront.

Lender requirements vary

How a van is classified matters. Some lenders treat Sprinters as commercial vehicles, others as recreational. Insurance requirements can slow down approval. Having clear documentation, dealer invoices, or proof of completed work can make the process smoother.

Reddit: Van owner discussion around private-party and custom builds often highlight how lender comfort and vehicle classification affect financing outcomes.

Structure and timing matter more than the financing itself

Most financing issues come down to how the purchase is structured and when things happen, not whether financing a van build is possible. There’s no single path that works for everyone, and separating van and build costs is normal.

Choosing the Right Financing Path for Your Build Goals

Financing a camper van build involves tradeoffs between structure, flexibility, and how much you want to own outright from the start. There’s no single setup that works for everyone. What matters is finding an approach that aligns with your goals and budget.

As a licensed dealer, Geotrek can support different financing structures depending on how your van and build are configured. For a detailed breakdown of financing options, lender types, and next steps, visit our camper van financing page.